Retired Americans are set for a modest increase in monthly payments as the Average Social Security Check 2026 rises to an estimated $2,071, according to projections from the Social Security Administration.

The 2.8 percent cost-of-living adjustment will begin in January and reflects easing inflation but persistent pressure on household budgets. Experts say the increase helps stabilize retiree income, though rising medical and housing costs may diminish its overall impact.

Average Social Security Check

| Key Fact | Detail / Statistic |

|---|---|

| 2026 COLA | 2.8% adjustment |

| Estimated Average Benefit | $2,071/month |

| Increase Over 2025 | About $56/month |

| Earliest Claiming Age | 62 (with permanent reduction) |

| Total Retirees Affected | 50+ million |

What the Average Social Security Check 2026 Means for Retirees

The new Average Social Security Check 2026 projection shows that retired workers will receive roughly $56 more per month starting in January. This brings the average benefit from about $2,015 in 2025 to approximately $2,071. While smaller than the record-setting increases of recent years, experts say it reflects a return to more stable inflation conditions.

According to the Social Security Administration (SSA), the 2026 increase is designed to preserve purchasing power for retirees as part of the annual cost-of-living adjustment (COLA). The agency emphasizes that COLA does not improve benefits beyond inflation—it simply prevents erosion of value.

How the Cost-of-Living Adjustment (KW3) Determines Payments

The COLA mechanism, established in the 1970s, ensures Social Security benefits keep pace with inflation. The adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a federal inflation measure that tracks the changing cost of goods and services for workers.

Key Drivers Behind the 2026 COLA

- A moderate rise in consumer prices during the third quarter of 2025

- Lower energy inflation compared with 2022–2023

- Higher medical and housing costs that disproportionately affect retirees

Inflation cooled during the second half of 2025, leading to a smaller COLA compared with recent years. However, analysts note that CPI-W may not fully reflect seniors’ typical spending patterns.

Dr. Elaine Howard, a senior economist at the nonpartisan Urban Institute, explained:

“Older Americans face distinctly different spending patterns than younger workers. Healthcare, prescription drugs, and housing represent a larger share of retiree expenses, and those sectors continue to rise faster than headline inflation.”

Why Some Retirees Receive More—or Less—Than the Average Social Security Check

Although the Average Social Security Check 2026 serves as a useful national benchmark, individual benefits vary widely.

Factor 1 — Lifetime Earnings (KW2)

Social Security calculates benefits based on the highest 35 years of inflation-adjusted taxable earnings. Higher-earning workers and those with stable, long-term careers receive higher benefits.

Factor 2 — Age at Claiming

Claiming benefits early, at age 62, permanently reduces monthly payments—sometimes by up to 30 percent.

Waiting until full retirement age (66–67 depending on birth year) yields the standard benefit, while delaying until age 70 increases the benefit through delayed retirement credits.

Factor 3 — Spousal and Survivor Benefits

Eligibility for spousal or survivor benefits can significantly impact monthly income, especially for individuals who spent years outside the workforce.

Factor 4 — Partial Work or Low-Earning Years

Workers with shorter careers or many low-earning years generally receive below-average benefits.

What the 2026 Increase Means for Retiree Income (KW4)

Modest Gains, Rising Costs

Monthly benefits rising to around $2,071 may help retirees manage everyday expenses, but the value of the increase is tempered by rising medical prices. Medicare Part B premiums, often deducted directly from Social Security payments, are projected to increase again in 2026.

A recent report from Kaiser Family Foundation (KFF) notes that medical inflation continues to outpace general consumer inflation, creating a “retirement affordability gap” for millions of seniors.

Housing Affordability Remains a Concern

Retirees living in states with steep property taxes, rental costs, or homeowners’ insurance premiums may find their COLA increase quickly absorbed by rising bills. The National Council on Aging estimates that more than 60 percent of retirees spend at least one-third of their income on housing.

Regional Variations Are Significant

The value of the Average Social Security Check 2026 differs greatly depending on where retirees live. High-cost states—New Jersey, New York, California, Connecticut—offer higher baseline benefits but also higher living expenses.

Expert Perspectives on the 2026 Social Security Outlook

Economists, policy analysts, and retirement researchers offer a measured view of the 2026 benefits outlook.

Federal Perspective

The SSA reiterated that the COLA formula is functioning as intended.

A spokesperson noted:

“The COLA ensures that Social Security beneficiaries do not lose purchasing power due to inflation. It is not meant to serve as a long-term enhancement of benefits.”

Academic Insight

Dr. Marcus Levin, a retirement policy researcher at Georgetown University’s Center for Retirement Initiatives, said:

“The 2026 increase is smaller than what retirees saw during the inflation surge of the early 2020s, but it’s more aligned with long-term inflation trends. Still, seniors relying heavily on Social Security may feel squeezed.”

Advocacy Groups

Organizations such as AARP continue to push for a shift toward the CPI-E, an inflation index designed to reflect older Americans’ spending habits more accurately.

Their spokesperson stated:

“The current inflation index underestimates true retiree expenses. Adjusting the formula would better protect older adults from financial hardship.”

What Retirees Should Do to Prepare for the 2026 Changes

Financial advisers recommend several steps retirees should take before the new payments begin:

1. Review the Updated SSA Statement

Retirees should confirm their updated benefit amount through the mySocialSecurity online portal or by reviewing mailed notices.

2. Recalculate Net Income After Medicare

Since many retirees pay Medicare Part B and D premiums directly from their checks, calculating net benefits is crucial.

3. Revisit Household Budgets

Financial planners suggest adjusting budgets to account for rising prescription drug prices, energy costs, and possible tax implications.

4. Evaluate Additional Income Streams

Advisers emphasize that Social Security should not be relied upon as the sole income source. Retirees should consider savings withdrawals, pensions, part-time work, or investment income.

Related Links

IRS Announces Major Updates for 2026 — What Taxpayers Should Start Preparing for Now

Social Security Update — New Deadline Set That Could Affect Your Future Payments

Challenges Ahead — The Bigger Picture Behind Social Security

Demographic Pressures

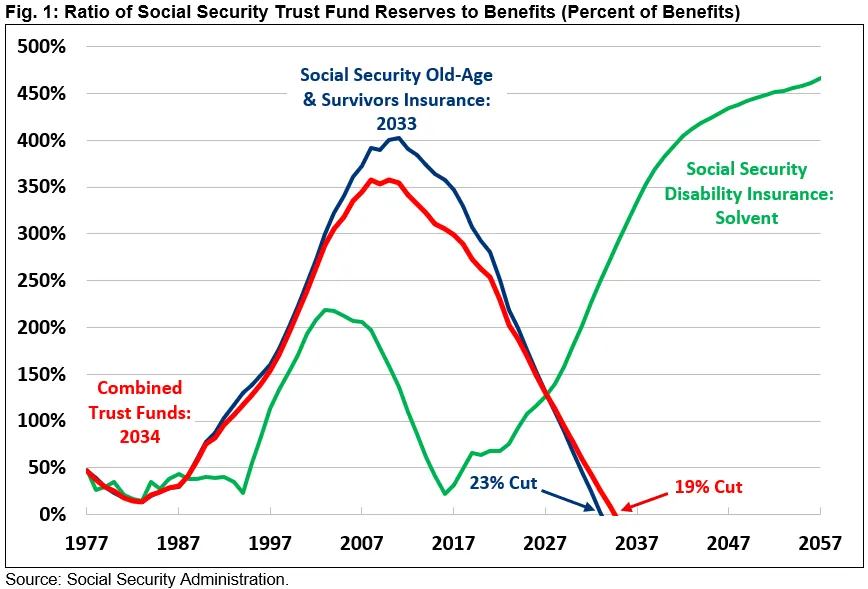

The U.S. population is aging rapidly. The ratio of workers to retirees continues to shrink, placing stress on the Social Security trust funds.

Funding Debate Intensifies

The Social Security Trustees Report projects that trust fund reserves may be depleted in the early 2030s without congressional intervention. If no action is taken, automatic reductions of up to 20–25 percent could hit future beneficiaries.

Policy Proposals Under Consideration

Lawmakers have suggested several approaches:

- Raising payroll tax caps

- Adjusting benefit formulas

- Increasing the full retirement age

- Adopting the CPI-E inflation measure

None have solid bipartisan support yet.

The Average Social Security Check 2026 reflects a modest but meaningful adjustment to retiree benefits amid a stabilizing inflation environment. While the increase helps maintain purchasing power, rising medical and housing expenses continue to challenge many households. As policymakers debate long-term reforms, retirees will need careful planning to secure financial stability in the years ahead.

FAQs About Average Social Security Check

1. What is the Average Social Security Check in 2026?

Approximately $2,071 per month for retired workers.

2. When do the new benefits begin?

January 2026 for Social Security; December 31, 2025 for SSI beneficiaries.

3. Will Medicare premiums reduce my increase?

Possibly. Medicare Part B premiums may rise, reducing net income.

4. Do all retirees receive the average amount?

No. Benefits vary widely based on earnings history, claiming age, and eligibility factors.

-

$33 Million Wells Fargo Subscription Billing Settlement: Who Qualifies and How

$33 Million Wells Fargo Subscription Billing Settlement: Who Qualifies and How

-

Pago del IRS de $2,000 por depósito directo en diciembre de 2025: guía de elegibilidad

Pago del IRS de $2,000 por depósito directo en diciembre de 2025: guía de elegibilidad

-

$400 Inflation Refund Checks for Everyone – 2025 December Payment Schedule

$400 Inflation Refund Checks for Everyone – 2025 December Payment Schedule

-

Cheques de estímulo de $1,000 para todos: calendario de pagos completo de 2025 para personas mayores

Cheques de estímulo de $1,000 para todos: calendario de pagos completo de 2025 para personas mayores