Criminal groups across the United States are increasingly using ATM skimming devices to steal debit-card information and personal identification numbers from unsuspecting consumers, according to federal law-enforcement agencies.

Despite advances in ATM security, the fraud method continues to evolve, allowing thieves to clone cards and withdraw cash within hours. Authorities warn that the crime remains one of the most persistent threats to everyday banking.

ATM Skimming Explained

| Key Fact | Detail / Statistic |

|---|---|

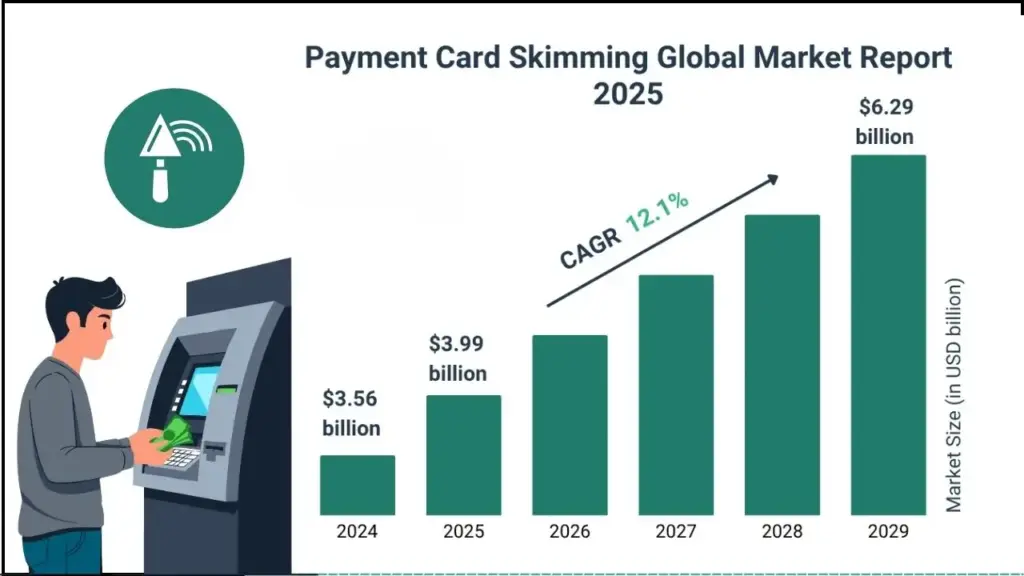

| Estimated annual global skimming losses | More than $1 billion |

| Devices most frequently targeted | ATMs, fuel pumps, POS terminals |

| Key information stolen | Card number, expiration date, PIN |

| Criminal objective | Card cloning, unauthorized withdrawals |

Understanding ATM Skimming

ATM skimming is a type of financial crime that relies on concealed hardware devices to capture card data from an ATM user. According to the Federal Trade Commission (FTC), skimming devices often resemble genuine ATM components and can be installed in less than a minute.

The collected information is used to produce cloned cards, which allow criminals to withdraw funds directly from victims’ accounts.The crime persists because of the continued reliance on magnetic-stripe technology, which is more vulnerable than modern chip-based authentication systems.

How Skimming Devices Are Installed

According to the U.S. Secret Service, which leads many ATM fraud investigations, skimming operations generally involve two hardware elements:

1. Card-Reader Skimmer

These are installed directly over the ATM’s card slot or inserted into the slot. Devices range from simple magnetic-stripe collectors to “deep-insert skimmers” only millimeters thick.

2. PIN-Capturing Tools

Thieves use one of the following:

- Hidden micro-cameras aimed at the keypad

- Fake keypad overlays that record keystrokes

- Shoulder-surfing techniques in crowded areas

Keypads often feel raised, loose, or spongy because they sit atop the real keypad.

3. Wireless Data Transmission

Modern skimmers often use Bluetooth or small 4G chips to transmit stolen information in real time. This reduces the risk of criminals needing to return to the machine.

Historical Evolution of ATM Skimming

ATM skimming first emerged in Europe in the late 1990s, according to a review published by Europol. Early devices were bulky and easier to detect. Over the last decade, skimmers have become significantly smaller due to improvements in microelectronics and 3D printing.

Key developments include:

- 2005–2010: Surge in external card-slot overlays

- 2011–2016: Introduction of deep-insert skimmers and keypad overlays

- 2016–2020: Rise of Bluetooth-enabled devices

- 2020–present: Introduction of “shimmers,” which target chip cards

The Secret Service reports that organized criminal groups often operate internationally, with devices assembled overseas and deployed in coordinated “skimming runs” across multiple U.S. states.

How Criminals Drain Accounts Using ATM Skimming

Once thieves collect card data, they follow a predictable sequence:

Data Extraction

Wireless skimmers send stolen data to a nearby receiver, often a concealed smartphone or laptop.

Card Cloning

Using inexpensive magnetic-stripe encoders, criminals write stolen data onto blank plastic cards.

Cash Withdrawal

Fraud groups typically target:

- High-traffic ATMs

- Low-surveillance convenience store machines

- ATMs near tourist areas or transportation hubs

The Department of Justice (DOJ) reports that some groups withdraw thousands of dollars within minutes of encoding each card.

Case Studies: Recent U.S. Incidents

Boston, Massachusetts (2023)

Federal prosecutors charged members of a Romanian fraud ring with installing deep-insert skimmers on ATMs in Boston and several neighboring cities. The DOJ reported more than $500,000 in losses before arrests were made.

Phoenix, Arizona (2022)

The Phoenix Police Department uncovered a multi-state operation involving Bluetooth-enabled shimmers placed inside chip readers at gas stations and ATMs. Investigators seized dozens of cloned cards.

Miami, Florida (2021)

The U.S. Secret Service reported an operation that placed skimmers in tourist-heavy neighborhoods. Losses exceeded $1.2 million, according to a federal affidavit. These cases illustrate that ATM skimming remains an adaptable crime driven by organized networks.

Warning Signs That an ATM May Be Compromised

Experts recommend a brief inspection before using any ATM. Warning indicators include:

- Loose or misaligned card readers

- Extra attachments near the screen or keypad

- Keypads that appear raised or unusual

- Visible camera holes near the keypad

- ATMs located in poorly lit or unsupervised areas

The FTC advises consumers to use indoor ATMs, especially those located in bank lobbies or monitored buildings.

Global Perspective on ATM Skimming

Skimming is not limited to the United States. The European Union Agency for Law Enforcement Cooperation (Europol) reports widespread targeting of ATMs in Spain, Italy, Romania, and the United Kingdom. In Asia, financial regulators in India, Malaysia, and the Philippines warn that deep-insert skimmers are increasingly common.

Global criminal markets play a role as well. Stolen data is sometimes sold on encrypted marketplaces, where buyers pay for ready-made card profiles that can be used internationally.

Economic Impact on Banks and Consumers

Financial institutions bear significant costs. A study from Javelin Strategy & Research estimates that skimming contributes meaningfully to the $10 billion in annual U.S. losses from card-present fraud. Banks must reimburse consumers, replace compromised cards, investigate incidents, and deploy new security technologies.

Who Gets Reimbursed?

Under U.S. regulations—including the Electronic Fund Transfer Act (EFTA)—consumers are typically refunded for unauthorized withdrawals if they report fraud promptly. However, delays in reporting may reduce reimbursement eligibility.

Expert Perspectives

Dr. Lena Hartwell, a cybersecurity researcher at Carnegie Mellon University, says the threat remains serious. “Skimming continues because the economics favor the criminals. The devices are cheap, the profits are high, and detection is difficult until after victims report losses,” she explained during a 2024 financial-security conference.

Meanwhile, Special Agent Matthew O’Neill of the Secret Service notes that criminals adapt quickly.

“Every improvement at the ATM level leads to a new workaround on the criminal side,” he said.

He emphasized the importance of public awareness and early reporting.

How Banks and Regulators Are Responding on ATM Skimming

Banks have introduced several protective measures:

- Anti-skimming jamming technology

- Randomized ATM software behaviors

- Reinforced card-slot construction

- Machine-learning systems that detect abnormal withdrawal patterns

In addition, federal regulators—including the Federal Reserve and the Office of the Comptroller of the Currency (OCC)—encourage banks to adopt stronger authentication methods and enhance surveillance at ATM locations.

Related Links

Two Social Security Payments Arriving This Week — One Group Receives an Extra Deposit

$725 Monthly Benefit Continuing Through 2026 — Check If You Qualify

Consumer Protection: Practical Steps

Experts recommend several steps to reduce risk:

- Inspect ATMs before insertion

- Cover the keypad while entering your PIN

- Use machines in monitored bank lobbies

- Enable withdrawal alerts via SMS or app

- Check statements frequently

- Report suspicious withdrawals immediately

The Future of ATM Security

As financial institutions transition toward contactless and cardless ATM withdrawals, skimming opportunities may decline. However, analysts caution that fraud networks will likely shift toward new attack vectors, including QR-code manipulation and mobile-banking exploits.

According to Dr. Hartwell, “Consumer education will remain essential. Technology reduces risk, but vigilance closes the gap.”